-

VRIGHT Exchange – Daily Digest posted an update in the group VRIGHT Exchange | Daily Digest: Corporate & Economy

6 months agoVRIGHT Exchange – Daily Digest | Corporate & Economy Analysis for September 12, 2025

Market Summary & Sentiment

• Indian markets opened higher:

o Nifty 50 up ~0.28% at ~25,074

o Sensex up ~0.26% at ~81,759

• This extended an 8-session rally, amid renewed confidence in potential U.S. Fed rate cuts, thanks to softer jobs data offsetting higher inflation .• Foreign portfolio inflows likely to remain strong as emerging markets like India benefit from lower U.S. yields . Domestic institutions continued their buying streak.

Sector Highlights & Corporate Actions

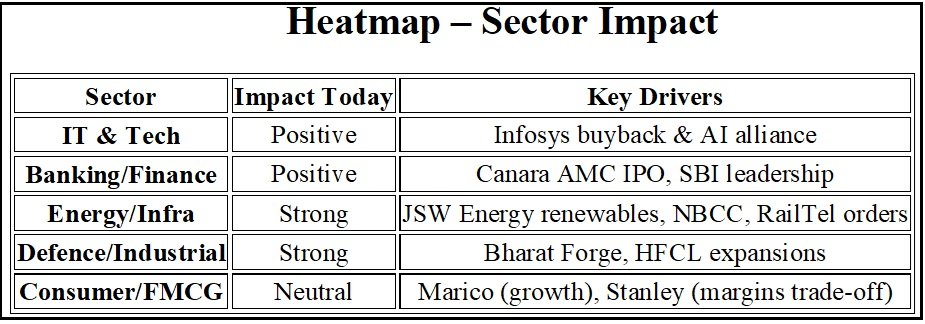

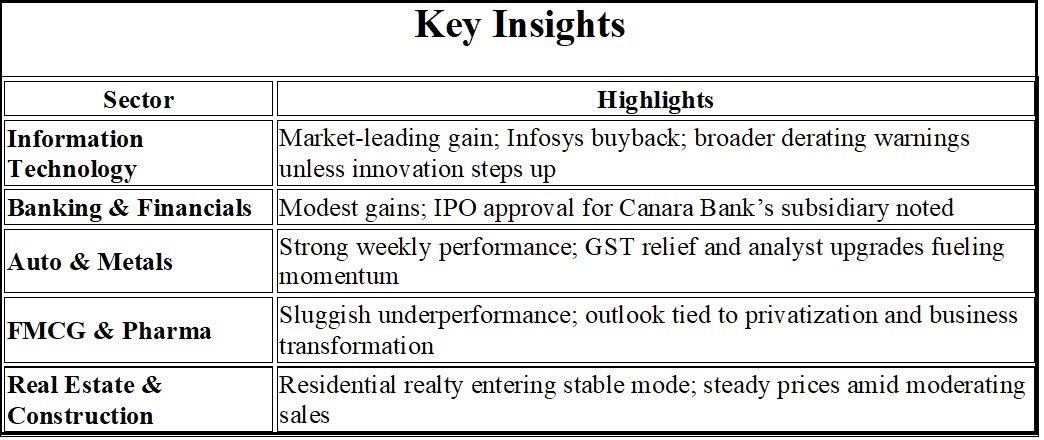

Information Technology (IT)

• IT index outperformed, gaining ~1%, led by a ~2% surge in Infosys following board approval of its largest-ever $2.04B share buyback at a ~19.2% premium .

• Earlier concerns were noted about potential derating in IT, unless the sector adapts and innovates—highlighted by industry analyst Manish Chokhani .

Banking & Financials

• Banking stocks had modest gains, part of broad-based sectoral appreciation.

• Canara Bank’s subsidiary got IPO approval, noted as a key corporate catalyst .

Auto & Metals

• Both sectors showed strength in the week leading up to Friday.

o Autos benefitted from earlier GST-led price cuts (e.g., Tata Motors),

o Metals rallied on upgrades by analysts on firms like JSW, Tata Steel,

SAIL .

• Sector trend continued into Friday, contributing to broad gains .Consumer: FMCG & Pharma

• The FMCG and pharmaceutical sectors viewed as lagging unless strategic revamp occurs—slower growth trends highlighted by Chokhani .Real Estate & Construction

• ICRA projects residential real estate entering a stabilizing phase, with sales volumes moderating and prices expected steady in FY26 .Macro & Global Developments

• Global cues: Asian markets rallied on Fed-cut optimism while oil prices dipped on weaker demand signals .

• Softer U.S. labour data lifted rate-cut expectations, overshadowing hotter U.S. inflation readings from August .

• Continued easing in goods & services tax (GST) and improving India-U.S. trade optimism further supported sentiment .Specific Corporate Moves & Regulatory Notes

• Infosys buyback dominance remains the headline corporate event of the day—largest in its history, boosting market wide IT traction .

• Cohance Lifesciences cleared a U.S. FDA audit with zero observations, providing a positive regulatory signal for pharma exports .

• Broader corporate governance and regulatory updates remain quiet today; no landmark regulations or policy announcements reported.Sector Weekly Trends

According to a recent survey, over the past week:

• 18 of 20 major sectors posted gains; only IT and Chemicals posted flat or negative returns

• Metals, Autos, Capital Markets, Consumer Durables, NBFCs led winners—each gaining over 3%

• Average sector return stood at ~1.85% .Outlook & Outlook

• Market sentiment remains upbeat, driven by U.S. Fed rate-cut bets, improving trade outlook, and sustained domestic institutional buying.• Infosys buyback continues to offer strong positive ripple effects, especially across IT.

• Watch for August inflation numbers, potential new regulatory directives, and updates on U.S.–India trade developments that could influence coming sessions.

• Sector rotation may favor cyclicals like Metal, Auto, and Capital markets, while structural challenges persist in FMCG, IT and pharma unless they pivot strategically.

Top Corporate Developments

• Infosys – Approved a ₹18,000 crore buyback (2.41% equity) and entered a 10-year AI-first alliance with HanesBrands. This reflects strong balance sheet confidence and an intent to deepen global retail partnerships. Likely to provide near-term earnings accretion.

• Bharat Forge – Partnered with Windracers for UAV operations and secured a landmark export contract with UAE’s MP3 International for howitzer barrels. Strengthens its presence in defence manufacturing with long-term growth implications.

• Lodha Developers – Signed a ₹30,000 crore MoU with the Maharashtra government to build a green integrated data centre park in Palava. A diversification into digital infrastructure, execution will be the key variable.

Banking & Financial Services

• Canara Bank – Subsidiary Canara Robeco AMC received SEBI clearance for filing its IPO prospectus. This could unlock value and strengthen Canara’s capital position.• State Bank of India – Ravi Ranjan recommended by FSIB as the new Managing Director. Leadership transitions at SBI often signal subtle shifts in credit growth and risk approach.

Energy & Infrastructure

• JSW Energy – Added 317 MW of renewable capacity (hydro, solar, wind), taking total installed base to 13,097 MW. Reinforces its position as a key green energy player.• NLC India – MoU signed with Khanij Bidesh India to develop projects in critical and strategic minerals, aligning with India’s EV and clean-tech ambitions.

• Insolation Energy – Incorporated four SPVs for solar power projects, pointing to pipeline expansion.

• NBCC India – MoU with RIICO for the ₹3,700 crore Rajasthan Mandapam project near Jaipur airport, enhancing its order book.

• JSW Infrastructure – Acquired a brownfield rail siding in Ballari for ₹57 crore. Strengthens logistics integration with group steel operations.

• RailTel Corporation – Secured two municipal contracts worth a combined ₹103 crore, reflecting steady traction in smart city projects.

Consumer & Lifestyle

• Marico – Acquiring the remaining 46.02% in HW Wellness Solutions (True Elements). Positions Marico more firmly in health foods, a high-growth FMCG segment.• Stanley Lifestyles – Announced festive-season price reductions across Sofas & More outlets to drive sales volumes. Positive for demand capture, though near-term margins may be affected.

Industrial & Defence

• HFCL – Received approval for 1,000 acres in Andhra Pradesh to establish defence manufacturing facilities. A significant capacity expansion aligned with national security priorities.• Mahindra & Mahindra – Through Mahindra Holdings, acquired full stakes in Contech and PSL Media & Communications. A group consolidation exercise with limited short-term financial impact.

VRIGHT Exchange Perspective

• Technology: Infosys’ buyback could set a precedent in the IT sector; watch peer responses.

• Defence: Bharat Forge and HFCL underline defence as a structural growth theme, both for exports and domestic demand.

• Energy: Strong momentum in renewables and minerals suggests long-term sectoral tailwinds.

• Banking: The Canara AMC IPO and SBI’s leadership change highlight an active phase for financial services.

• Consumer: Festive demand strategies (Marico, Stanley) will be an early gauge of discretionary spending ahead of Q3.

-

VRIGHT Exchange – Daily Digest posted an update in the group VRIGHT Exchange | Daily Digest: Corporate & Economy

6 months ago